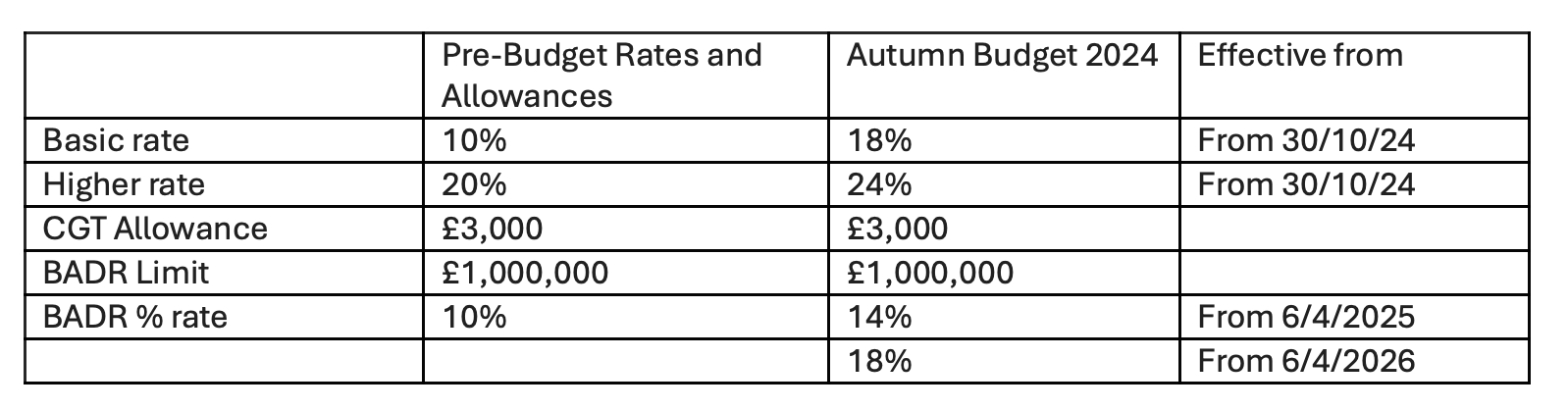

Rachel Reeves confirmed an increase in the rate of CGT to apply for disposals made on or made after 30 October 2024.

The actual rise was not as high as many were expecting, and rather than aligning CGT rates to income tax rates, instead there was an alignment of rates to the current CGT rates on the sale of residential property.

All capital gains from budget day will therefore be subject to tax at either 18% or 24%. For higher rate taxpayers (which most gains fall into) this is a rise of 4%, whereas basic rate taxpayers suffer an 8% increase in their rate of CGT.

The impact for trustees and personal representatives is a CGT rate rises from the current rate of 20% to 24%.

The £1m cap for Business Asset Disposal Relief (BADR) remains unchanged however the current 10% tax rate will increase to 14% from 6th April 2025 and 18% from 6th April 2026.

Changes at a glance

What didn’t change?

There were no changes to the CGT allowance, which currently stands at £3,000 for individuals and £1,500 for trusts.

No change in the rate of CGT on the sale of UK residential property.

Capital gains on the sale of UK residential property will still need to be reported and paid under the 60-day reporting regime.

No change in the ISA allowance of £20,000 per annum.

Private client and personal tax

Private client and personal tax  Video Games Tax Credits

Video Games Tax Credits  Trusts, IHT and estate planning

Trusts, IHT and estate planning  Corporate tax

Corporate tax